Last Updated on: 13th July 2026 | Last Reviewed on: 13th July 2026

Key takeaways at a glance

- Who is covered: any individual holding a certificate of practice under section 6 of the Chartered Accountants Act, 1949, whether practising individually or through a firm, who carries out a notified financial transaction on behalf of a client (a “relevant person” under the Ministry of Finance Notification).

- The trigger: AML/CFT/CPF obligations is triggered when a chartered accountant is carrying out any of the specified financial transactions on behalf of a client, including buying or selling immovable property; managing client money, securities or other assets; managing bank, savings or securities accounts; organising contributions for the creation, operation or management of companies; and the creation, operation or management of companies, LLPs or trusts and the buying and selling of business entities.

- Governing laws: the PMLA 2002 and the PML (Maintenance of Records) Rules, 2005(PMLR); the AML/CFT Guidelines for ICAI, ICSI and ICMAI professionals, 19 June 2023; the UAPA 1967 (Section 51A) and the WMD Act, 2005 (Section 12A).

- Supervisor: the Institute of Chartered Accountants of India (ICAI). Reports are furnished to the Financial Intelligence Unit – India (FIU-IND); the Enforcement Directorate (ED) enforces the PMLA.

- Core duties: registration with FIU-IND, an internal risk assessment, customer due diligence and KYC, beneficial-owner identification, ongoing monitoring, suspicious transaction reporting, five-year record-keeping and sanctions screening.

This guide is general information on Indian law, not legal advice. For your profession’s specific position, speak to a qualified AML professional.

Chartered accountants do not become reporting entities merely by practising their profession or holding the certificate of practice. They fall within the scope of the Prevention of Money Laundering Act 2002 only when, in the course of practice and on behalf of a client, they undertake the specified financial transactions notified by the Ministry of Finance.

The trigger is therefore the nature of the professional engagement rather than the profession itself. Once a member holding a certificate of practice performs one of the notified transactions for a client, the AML, CFT and CPF duties flow from the PMLA, the PML (Maintenance of Records) Rules, 2005, the AML and CFT Guidelines issued jointly for the ICAI, ICSI and ICMAI professionals, the UAPA, the WMD Act and the FIU-IND reporting framework.

The core instruments at a glance

| Instrument | What it does for a CA in practice |

| PMLA, 2002 | Treats chartered accountant as reporting entity and establishes core duties of risk assessment, record-keeping and reporting. |

| PML (Maintenance of Records) Rules, 2005 | Set out what to report and when, how to identify clients and beneficial owners, and the duty to appoint officers. |

| S.O. 2036(E), 3 May 2023 | The notification that lists the specified financial transactions and defines the relevant person. |

| AML/CFT Guidelines for ICAI, ICSI, ICMAI (19 June 2023) | The relevant person’s working rulebook, issued jointly for the three professions. |

| UAPA Section 51A and WMD Act Section 12A | Impose targeted financial sanctions for terrorism and proliferation financing on a relevant person. |

| FATF Recommendations 22 and 23 | The international standards for DNFBPs that India’s professional regime is built to meet, supported by the FATF accounting profession guidance of 2019. |

When is a chartered accountant covered by the PMLA?

Chartered Accountants are only classified as reporting entities under the PMLA when, in the course of practice and on behalf of a client, they carry out one of five specified financial transactions. These transactions include buying or selling any immovable property; managing client money, securities or other assets; managing bank, savings or securities accounts; organising contributions for the creation, operation or management of companies; operation, creation, or management of companies, limited liability partnerships (LLPs) or trusts, and buying and selling of business entities.

The distinction is important in practice. Statutory audit, tax audit, certification and attestation service, representation before authorities and ordinary compliance filings do not by themselves trigger reporting entity obligations. Rather, it is the handling or arrangement of a client’s money, assets, accounts or corporate vehicles that brings a certificate holder within the scope of law, as that is where a professional can, knowingly or unknowingly, facilitate the movement, placement or concealment of illicit funds.

Are chartered accountants reporting entities under the PMLA?

Yes, the Prevention of Money Laundering Act, 2002 extends the reporting entity framework to Chartered Accountants through the Ministry of Finance Notification S.O. 2036(E) of 3 May 2023. Under this notification, a certificate of practice holder is treated as a relevant person when undertaking the specified financial transactions on behalf of a client in the course of practice. Accordingly, such a chartered accountant falls within the definition of reporting entity under section 2(1)(wa) of the PMLA as the notified transactions are prescribed under the residual sub-clause (vi) of section 2(1)(sa).

Once covered, a chartered accountant must register with FIU-IND and implement an AML, CFT and CPF compliance programme proportionate to the nature of the specified activities undertaken. This places a practising CA in the same broad group of reporting entities that file with FIU-IND as banks and other professionals, and connects the member to the wider set of DNFBPs subject to the PMLA. From that point, effective compliance depends not only on understanding the legal obligations but also on avoiding the common AML compliance mistakes that arise in practice.

Supervisory authority for chartered accountants in India

The supervisory body for chartered accountants is the Institute of Chartered Accountants of India (ICAI). It grants a certificate of practice to eligible individuals and issues guidelines to facilitate compliance with the AML, CFT, and CPF framework. In addition, the ICAI promotes awareness of ML, TF, and PF risks and supervises compliance with the principles prescribed in the PMLA and PMLR. Where a relevant person fails to comply with the norms and standards, the ICAI may take appropriate disciplinary action.

A relevant person must submit all prescribed reports through the ICAI with the Financial Intelligence Unit – India, which receives, analyses and disseminates them, while the Enforcement Directorate investigates and prosecutes the offence of money laundering under the PMLA.

Onboarding clients without a documented due-diligence process?

AML India can put client due diligence, beneficial-ownership checks and suspicious-transaction reporting in place for your practice, keeping you audit-ready without slowing your engagements down.

AML requirements for accountants: when the PMLA applies

The AML requirements for accountants in India turn on what the accountant actually does for a client. Under the notification of 3 May 2023 issued under Section 2(1)(sa) of the PMLA, a chartered accountant in practice becomes a reporting entity when they carry out specified financial transactions on a client’s behalf, such as managing the client’s money, securities or bank accounts, organising contributions for the creation or management of companies, or buying and selling immovable property or business entities. Audit, assurance and tax representation are not, on their own, covered. Knowing that line is the first of the anti money laundering checks for accountants, because it decides whether the full compliance framework is switched on.

Anti money laundering guidance for the accountancy sector

Once covered, a chartered accountant follows the same core duties as any reporting entity, tailored to a professional practice. That means registering with FIU-IND, appointing a Principal Officer and a Designated Director, running customer due diligence that confirms both the client and the beneficial owner, and keeping identity and transaction records for five years under Rule 10 of the PML (Maintenance of Records) Rules, 2005. Suspicious transactions are reported to FIU-IND within seven working days. The joint anti money laundering guidance for the accountancy sector issued by the ICAI on 19 June 2023 is the profession’s reference point and should be read alongside the PMLA and the Rules.

Practical anti money laundering checks for accountants

The accountants AML guidance translates into a short set of repeatable checks. Before onboarding, verify the client’s identity on officially valid documents, establish the purpose of the engagement, and identify anyone who ultimately owns or controls the client. During the engagement, watch for the red flags the ICAI lists, such as unusual cash movements, over complicated structures with no commercial rationale, or a reluctance to provide beneficial ownership detail. These anti money laundering checks for accountants, applied consistently and documented, are what an inspection will look for.

AML Regulatory Requirements for Chartered Accountants in India

The legal framework governing a chartered accountant acting as a relevant person is spread across multiple sources rather than a single law. It comprises the core legislation, the overarching regulatory obligations, the sectoral supervisor and its guidelines, the miscellaneous official reports, the international standards, and the allied laws. Each category of instruments plays a distinct role in defining the obligations of a CA who becomes a reporting entity under PMLA.

The framework is built around the PMLA as the principal legislation. The PML(Maintenance of Records) Rules, 2005 outline operational duties of reporting entities, while the notification S.O. 2036(E) brings chartered accountants into the framework when they undertake the specified financial transactions.

The joint professional Guidelines translate the statutory requirements into practical compliance measures for certificate holders. The UAPA and the WMD Act add counter-terrorism and proliferation financing sanctions, while the allied laws, including the Chartered Accountants Act, 1949, provide the broader professional context.

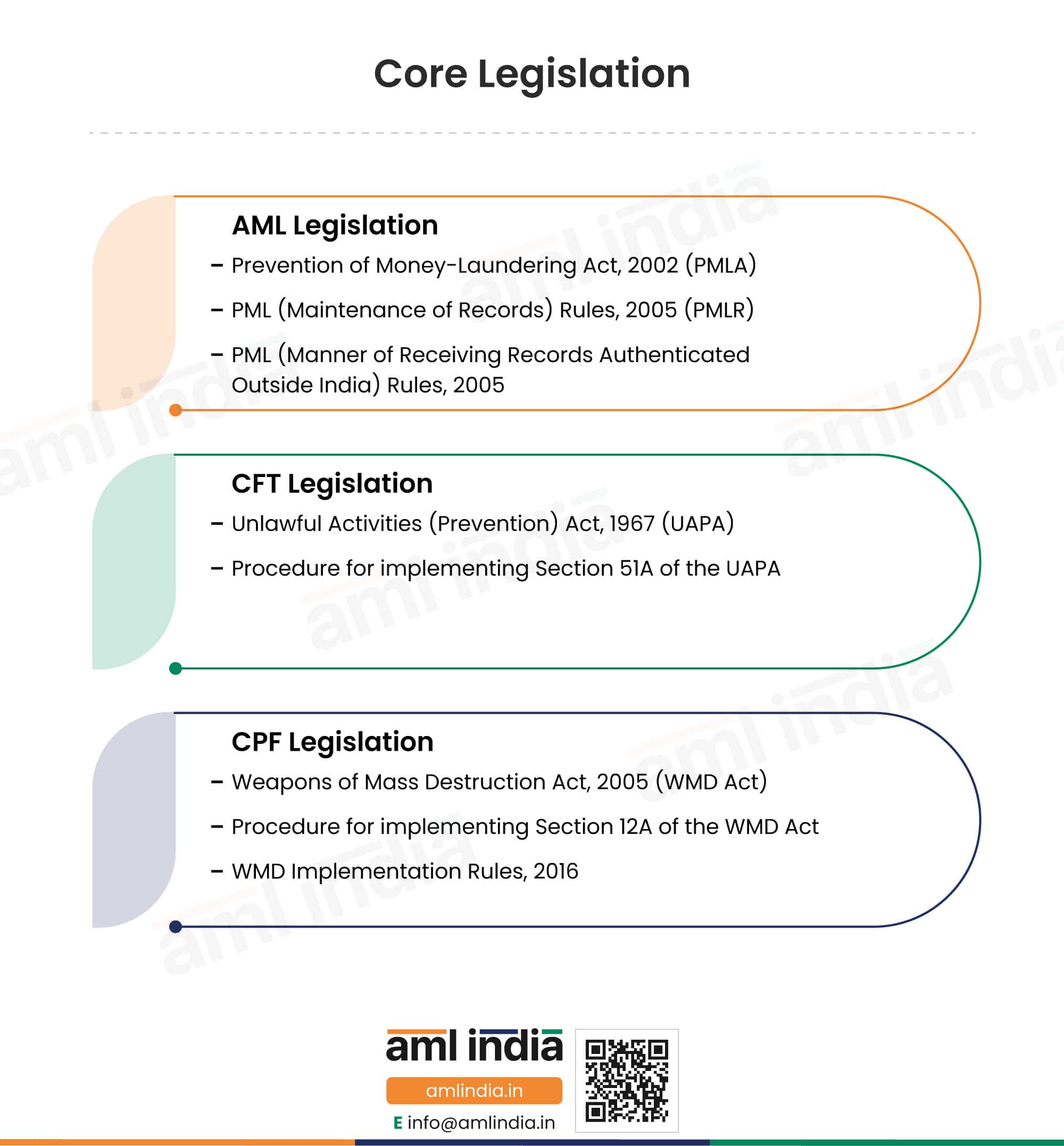

Core Legislation

The core statutes and rules governing the AML, CFT and CPF obligations are organised into three distinct categories.

AML Legislation

Prevention of Money-Laundering Act, 2002 (PMLA)

India’s principal anti-money laundering statute and the source of a relevant person’s reporting entity status. It defines the offence of money laundering and imposes obligations on reporting entities, including customer due diligence under Section 11A and manner of furnishing information under Section 15, that a chartered accountant must apply whenever a notified financial transaction is carried out on behalf of a client. The Act applies to the profession because a certificate holder who manages a client’s money, assets or corporate vehicles occupies a position where illicit funds can be placed or moved under the guise of professional legitimacy.

The PML (Maintenance of Records) Rules, 2005 (PMLR)

The operational rulebook made under the PMLA that translates the Act into practical compliance obligations. It prescribes the categories of transactions that must be recorded (Rule 3 and 4) the manner in which those records are to be maintained (Rule 5), the circumstances in which clients and beneficial owners must be identified (Rule 9), and the obligation to establish a mechanism for detecting suspicious transactions (Rule 7(3)).

The PMLR has been amended from time to time to respond to evolving financial crime risks. These amendments are reflected in 31 Gazette notifications and orders, set out below in a chronological legal history timeline.

| Gazette notification and date | Key change or rule touched |

| G.S.R. 389(E), 24 May 2007 | The earliest amendment to the 2005 Rules. It strengthened the reporting framework by broadening the scope of suspicious transaction under rule 2 to screen transactions lacking a legitimate economic purpose and transactions associated with terrorism financing. It further brought cash transactions involving forged or counterfeit currency within the scope of Rule 3, revised Rule 8 governing the furnishing of information to the Director and streamlined the compliance requirements under Rule 9 by requiring only one certified copy of listed documents. |

| G.S.R. 816(E), 12 November 2009 | A comprehensive revision of the 2005 Rules. It expanded the scope and introduced the definition of Regulator, revised the treatment of suspicious transaction, and introduced a reporting obligation for receipts exceeding Rupees 10 lakh received by NPO. It Further prescribed a ten-year retention period under Rule 6. |

| G.S.R. 76(E), 12 February 2010 | Revised Rules 3, 4, 5 and 7 to strengthen record-keeping framework and clarify the reporting requirements. A significant change was the introduction of the first Explanation in Rule 9(1A), which defines the beneficial owner as the natural person who ultimately owns or exercises controls over a client or on whose behalf a transaction is undertaken. |

| G.S.R. 508(E), 16 June 2010 | Introduced further revisions to Rules 2, 9 and 10, the governing definitions, customer due diligence and record keeping requirements. The amendment refined the customer identification and the supporting documents to be maintained by reporting entities, reflecting the continuing efforts during 2010 to tighten the CDD and record keeping regime. |

| G.S.R. 980(E), 16 December 2010 | The amendment introduced definitions of the Designated Officer and the small account, including limits on credits and account balance. It also expanded the list of officially valid documents under Rule 2 to include NREGA job card and the Aadhaar letter and inserted Rule 9(2A) prescribing operational limits of small accounts. |

| G.S.R. 481(E), 24 June 2011 | Adopted a short title of the rules. By amending Rule 1, the notification replaced the original descriptive title with the Prevention of Money-Laundering (Maintenance of Records) Rules. |

| G.S.R. 576(E), 27 August 2013 | Introduced significant revisions across Rules 2 and 3 and inserted new provisions after Rule 10 to reinforce reporting framework. It updated definitions, refined the treatment of cash and suspicious transaction reporting, expanded provisions relating to reporting entities and regulators, and modified the record keeping framework to ensure consistency with reporting obligations. |

| G.S.R. 288(E), 15 April 2015 | Revised the definitions in Rule 2 to update the scope and interpretation of key terms used throughout the rules. As the definitions determine the application of the substantive provisions. |

| G.S.R. 544(E), 7 July 2015 | Amended Rules 2, 9 and 10 to strengthen the customer due diligence and record-keeping framework. It also clarified how a reporting entity identifies clients and what it preserves. |

| G.S.R. 730(E), 22 September 2015 | It revised the reporting framework by requiring the director to specify reporting procedures and formats in consultation with the relevant regulator and clarified validation of official documents even after name change. |

| G.S.R. 882(E), 18 November 2015 | Amended the definitions and reporting provisions, explanting how key terms are understood and how transactions reach the FIU and ending the 2015 sequence of amendments. |

| G.S.R. 347(E), 12 April 2017 | Revised Rule 2 and added Rule 9A, inserting the Central KYC Records Registry into the Rules, creating the duty to file client KYC records centrally and the basis to revive them, the structural addition that underpins today’s CKYCR. |

| G.S.R. 538(E), 1 June 2017 | Amended Rules 2 and 9 to insert Aadhaar in customer due diligence, prescribing Aadhaar-based identification and authentication for KYC, an approach subsequently reshaped by the Supreme Court’s Aadhaar ruling. |

| G.S.R. 1038(E), 21 August 2017 | Amended the Rule 2 definitions, updated the scope and interpretation of key terms that determine the application of the reporting requirements. |

| G.S.R. 1318(E), 23 October 2017 | A later 2017 recalibration of the Rule 2 definitions, holding the defined terms current as the framework progressed. |

| G.S.R. 456(E), 16 May 2018 | Revised the definitions and customer due diligence provisions, clarifying coverage and how clients are identified and verified, within the ongoing adjustment of the CDD framework. |

| G.S.R. 1078(E), 31 October 2018 | Amended Rule 9 on customer due diligence, strengthening the steps a reporting entity follows to identify and verify clients and beneficial owners, one of a series of Rule 9 changes over 2018 and 2019. |

| G.S.R. 108(E), 13 February 2019 | Revised Rules 2 and 9 on definitions and customer due diligence, in the wake of the legislative changes to Aadhaar use, revising the ways identification could be conducted. |

| G.S.R. 381(E), 28 May 2019 | Amended Rule 9 to refine the identification and verification process and the modes to confirm a client’s identity, part of the post Aadhaar reshaping of CDD. |

| G.S.R. 582(E), 19 August 2019 | Amended Rules 2 and 9 and inserted additional provisions after Rule 11, strengthening the customer due diligence and record keeping framework. It also mentioned about maintenance and sharing of KYC information by reporting entities one of the broader 2019 revisions. |

| G.S.R. 669(E), 18 September 2019 | Inserted definitions under Rule 2 and sharpening the customer due diligence process and beneficial owner identification under Rule 9 within the 2019 series of CDD amendments. |

| G.S.R. 840(E), 13 November 2019 | Revised Rule 9 with further refinements to the identification and verification requirements, concluding the 2019 series of CDD changes. |

| G.S.R. 228(E), 31 March 2020 | Amended Rule 9 to extend the operational validity of small accounts, enabling reporting entities to continue operating such accounts during the prescribed period. |

| G.S.R. 251(E), 13 April 2020 | Revised Rule 8, which governs the furnishing of transaction reports to the FIU, sharpening the manner and content of what a reporting entity submits. |

| G.S.R. 254(E), 16 April 2020 | Further amended Rule 8 to revise the reporting timelines for specified transactions under Rule 3 improving the operational reporting process. |

| G.S.R. 798(E), 28 December 2020 | Amended Rule 2 to revise the definition of regulator by specifying the competent regulatory authorities for DNFBPs, thereby strengthening the supervisory framework. |

| G.S.R. 575(E), 13 July 2022 | Amended Rules 2 and 9A. It introduced definitions of IFSC, prescribed beneficial ownership requirements for IFSC entities, and modified the central KYC records registry framework under rule 9A to accommodate customers operating within the IFSC regime. |

| S.O. 1074(E), 7 March 2023 | Amended Rules 2, 3A and 9 to strengthen the definitions of politically exposed persons, non-profit organisations and group. Inserted Rule 3A duty for group-wide AML policies and reduced the company beneficial ownership threshold from 25 to 10 per cent, with a matching change to Rule 9(3)(e), so a member must look further into ownership. |

| G.S.R. 652(E), 4 September 2023 | The second major amendment of 2023 strengthened the governance, by requiring the Principal Officer to be at management level, reduced the partnership beneficial ownership threshold from 15 to 10 per cent, added an Explanation of control, obliged trustees to disclose their status, and required the results of any Rule 3 and Rule 9 analysis to be kept among the records. |

| G.S.R. 745(E), 17 October 2023 | Amended Rules 2, 3, 3A, 8 and 9 together, it enhanced definitions, beneficial ownership verification, customer due diligence and risk-based compliance measures. Also introduced group-wide policies and reinforced STR and confidentiality requirements. |

| G.S.R. 419(E), 19 July 2024 | Strengthened Rule 9(1C) by requiring entities to retrieve and use KYC Identifier instead of repeatedly collecting the same documents, except in specified circumstances. Also introduced a seven-day deadline to update a CKYCR record after any change and revised Rule 9A(2)(g) on filing, retrieving and using registry records, tightening how current central KYC data is maintained. |

The PML (Manner of Receiving the Records Authenticated Outside India) Rules, 2005

A concise set of rules governing the acceptance of client identification documents authenticated outside India. For a chartered accountant, they apply when a notified transaction involves a non-resident client or a foreign entity, and relies on customer identity or beneficial ownership documents that have been executed and authenticated abroad rather than in India.

CFT Legislation

The Unlawful Activities (Prevention) Act, 1967 (UAPA)

India’s principal counter-terrorism statute. Section 51A of the Act requires a relevant person to screen clients and beneficial owners against the designated terrorist lists and to freeze, without delay, the funds and assets of any designated person or entity. These obligations apply whenever a chartered accountant undertakes a notified financial transaction on behalf of a client.

Procedure for implementation of Section 51A of the UAPA (order dated 2 February 2021; corrigendum dated 15 March 2023)

The official systematic procedure a certified chartered accountant follows to give effect to Section 51A when a client matches a designated list. It prescribes the steps for sanctions screening, freezing of assets and reporting. The joint professional Guidelines for chartered accountants integrate these requirements into day-to-day compliance procedures, translating the statutory obligations into a practical implementation framework.

CPF Legislation

The Weapons of Mass Destruction and their Delivery Systems (Prohibition of Unlawful Activities) Act, 2005 (WMD Act)

India’s counter-proliferation financing legislation. Section 12A establishes the legal background for implementing targeted financial sanctions relating to the financing of weapons of mass destruction, and it reaches a relevant person because professional services in managing money or forming entities can be used to move value for a sanctioned network.

Procedure for implementation of Section 12A of the WMD Act (dated 1 September 2023)

The implementation procedure for Section 12A mirrors the Section 51A screening and freezing steps but for proliferation financing designations. For a relevant person, it is applied through the same joint professional Guidelines, so terrorism and proliferation designated lists are both checked in the notified engagements.

The WMD and their Delivery Systems (Prohibition of Unlawful Activities) Implementation Rules, 2016

The subordinate rules that put the WMD Act into operation and support the list-handling, freezing and reporting actions a relevant person must be able to carry out when a proliferation-financing designation match arises in an engagement.

Not registered with FIU-IND yet, or unsure whether you have to be?

AML India can confirm whether your firm qualifies as a reporting entity under the PMLA, complete your goAML registration and appoint your principal officer and designated director.

Overarching Obligations

The applicable obligations that a relevant person complies with once a notified engagement makes the certificate holder a reporting entity.

CERSAI Central KYC Records Registry (CKYCR) Operating Guidelines, 2025

The Central KYC Records Registry is the repository for receiving, storing and retrieving the KYC records. For Chartered Accountants undertaking a financial transaction as a relevant person, the registry facilitates the upload of the client’s verified KYC record and the retrieval of existing KYC records. The 2025 guideline set out the procedure for maintaining KYC records through the registry, helping chartered accountants ensure consistency in CDD and compliance with PMLA and PMLR.

FINnet 2.0 reporting formats (2024) and the FINGate 2.0 reports manual (June 2023)

The FIU-IND reporting platform, the 2024 reporting formats and the FINGate 2.0 user manual provide an operational framework for a chartered accountant, acting as a relevant person to enrol as a reporting entity and submit prescribed reports to FIU-IND. They provide the enrolment process, reporting formats and filing procedures required to comply with the reporting obligations under the PMLA and the PMLR.

Section 11A Aadhar authentication procedure for non-banking entities

Prescribes the procedure for non-bank reporting entities to obtain authorisation to use Aadhaar authentication for CDD. A chartered accountant relevant person must apply through ICAI, which forwards the application to UIDAI; only after the authorisation, the chartered accountant can use Aadhaar authentication to verify a client’s identity.

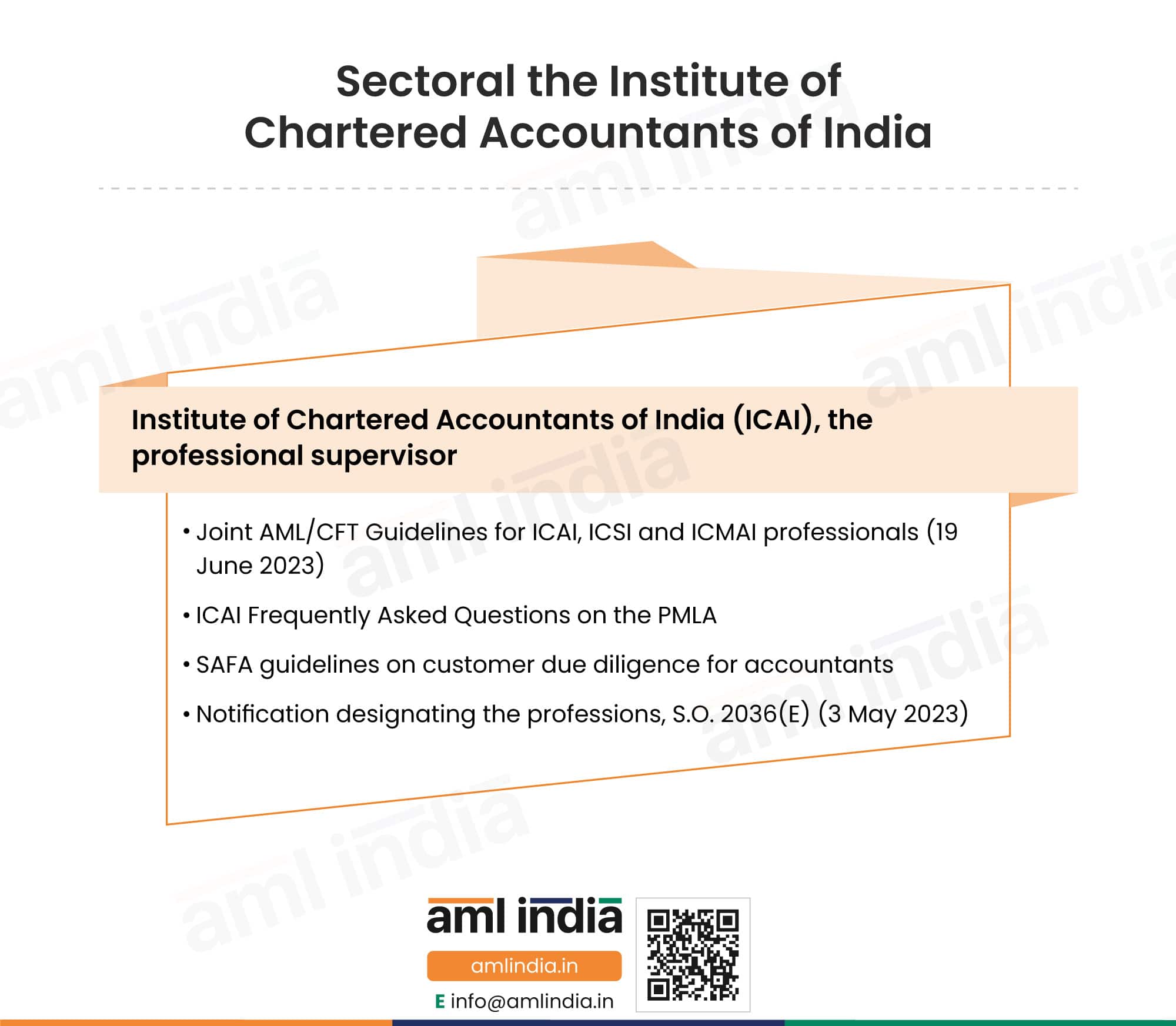

Sectoral Framework

The professional supervisor and its guidelines. This is the layer that gives the chartered accountant regime its own character. The ICAI is the statutory body supervisor, FIU-IND receives reports, and ED investigates.

AML/CFT Guidelines for professionals with certificates of practice from ICAI, ICSI and ICMAI (19 June 2023)

The relevant person’s primary compliance framework. Issued jointly for the members of ICAI, ICSI and ICMAI, the Guidelines explain when a professional becomes a relevant person and set out AML, CFT and CPF obligations, including establishing internal policies and procedures, customer due diligence, officially valid documents, beneficial-owner identification, transaction monitoring, suspicious transaction reporting, record-keeping, the appointment of a Designated Director and Principal Officer, and the implementation of Sections 51A and 12A of UAPA and WMD respectively. Where this article states a duty at the level of the law, the Guidelines are where a member finds the detail.

ICAI Frequently Asked Questions on the PMLA

The ICAI’s own question-and-answer guidance for members, which explains in practical terms when a chartered accountant is a relevant person, which engagements are caught, and how the obligations apply to a practice. It is a useful companion to the joint Guidelines for day-to-day judgement calls.

SAFA guidelines on customer due diligence for accountants

Guidance from the South Asian Federation of Accountants on customer due diligence for the accounting profession. It provides practical guidance on implementing a risk-based approach to customer due diligence, beneficial ownership and other measures. It complements the domestic AML, CFT and CPF Guidelines by promoting good practices for chartered accountants undertaking relevant person engagement.

Notification designating the professions, S.O. 2036(E) (3 May 2023)

The instrument that brings the specified financial transactions within the scope of section 2(1)(sa)(vi) of the PMLA. It defines a relevant person by reference to a certificate of practice under section 6 of the Chartered Accountants Act, 1949. Thereby determining when a CA is subject to PMLA as a reporting entity.

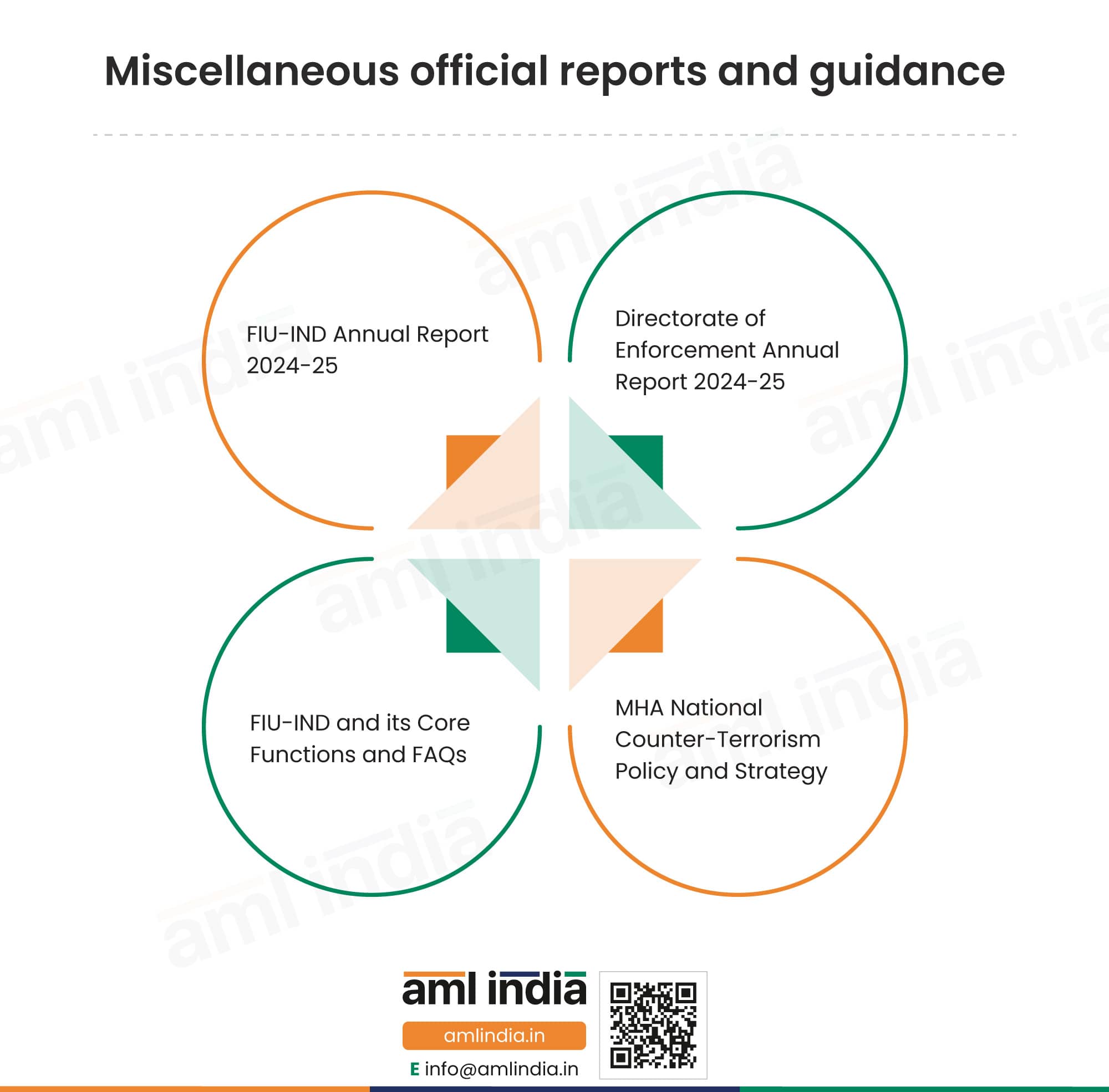

Miscellaneous official Reports and Guidance

Official reports and guidance that sit outside the binding rulebook but shape how a relevant person reads risk and duty.

FIU-IND Annual Report 2024-25

The report received, analysed and disseminated, accounts under PMLA. It provides insights into reporting trends, emerging ML, TF and PF typologies, and the implementation of AML obligations across reporting entities. For chartered accountants, it helps identify FIU-IND’s areas of supervisory focus and supports the strengthening of reporting and compliance practices.

Directorate of Enforcement Annual Report 2025-26

The report summarises the Enforcement Directorate’s investigation, prosecutions and convictions under the PMLA. It highlights money laundering cases, including cases involving professionals and corporate structures. For chartered accountants, the report serves as the practical reference for understanding enforcement trends and strengthening AML compliance.

FIU-IND and its Core Functions and FAQs

An explanatory report on the role of FIU-IND and the reporting framework under PMLA, it outlines how reporting entities enrol on FINnet 2.0, submit prescribed reports and interact with FIU-IND. For Chartered accountants, it serves as an introduction to establishing their reporting functions, understanding the FIU-IND’s expectations and the implementation of their reporting obligations.

MHA National Counter-Terrorism Policy and Strategy

The policy and strategy outline India’s strategic approach to preventing and combatting terrorist activities, including measures to disrupt terrorist financing. For chartered accountants, it provides the broader policy context for the counter-terrorism and financing obligations under UAPA and also the implementation of targeted financial sanctions under section 51A.

International Standards

The global benchmarks India is measured against, and the sources a certificate holder can use to calibrate a risk-based approach to the notified engagements.

FATF Recommendations

The international standards for combatting money laundering, terrorism and proliferation financing. Recommendations 22 and 23 extend AML, CFT and CPF obligations, including CDD, suspicious transaction reporting, record keeping and other preventive measures to chartered accountants, while Recommendation 6, updated in June 2026, sets the framework on targeted financial sanctions. India’s approach and framework for chartered accountants is built to meet these standards.

FATF Mutual Evaluation Report on India, 2024 and Executive Summary

The report was furnished following an assessment of India’s AML, CFT and CPF framework against the international standards. It reviewed the implementation of AML obligations for DNFBPs, including the accounting professionals, particularly in relation to supervision, CDD and reporting. It also mentions the scope for improvement of India’s framework and its implementation.

FATF Risk-Based Approach Guidance for the Accounting Profession,2019

Sector-specific FATF guidance on the money-laundering and terrorist-financing risks accountants face in the services they provide, and how a risk-based approach applies to the profession. It is a ready-made template for a certificate holder’s internal risk assessment.

Allied Laws

The wider body of law that defines the predicate offences and the enforcement machinery around money laundering, together with the statutes that govern the profession itself. A member does not administer the criminal and enforcement Acts, but they shape the risk to assess and the conduct that may need reporting.

The Chartered Accountants Act, 1949: Governs the chartered accountants and the ICAI. It supports the implementation of the AML, CFT and CPF framework by providing the professional regulatory and supervisory framework for chartered accountants acting as relevant persons.

The Chartered Accountants, the Cost and Works Accountants and the Company Secretaries (Amendment) Act, 2022: Strengthens the governance, disciplinary and oversight framework for the chartered accountants. It supports the implementation of AML, CFT and CPF framework through enhanced professional regulation and accountability..

The Companies Act, 2013: It governs the incorporation, management, governance and reporting of companies in India. Also provides for identifying significant beneficial ownership and maintenance of its register. A CA undertaking transactions on behalf of companies should ensure they take a risk-based approach and identify the UBO to ensure corporate structures are not manipulated to conceal illegal funds.

The Bharatiya Nyaya Sanhita, 2023 and the Bharatiya Nagarik Suraksha Sanhita, 2023: Provide the substantive criminal law and procedural framework for criminal offences in India. For chartered accountants, these laws provide the predicate offences and investigative framework that underpin money laundering under the PMLA. Accordingly, suspicious transactions should be assessed and reported where there are reasonable grounds to suspect that they involve proceeds of criminal activity.

The Foreign Exchange Management Act, 1999: Regulates foreign exchange transactions and cross-border movement of funds. CA’s acting on behalf of clients should ensure international money moves legally, comply with FEMA and report suspicious activity to FIUIND.

The Benami Transactions (Prohibition) Act, 1988: It provides for the identification, attachment and confiscation of benami transactions. CA’s exposed to benami transactions should verify the beneficial ownership of the client and assets.

The Prevention of Corruption Act, 1988: It criminalises corruption involving public servants and provides for the prosecution of corruption-related offences. CA’s should be alert to transactions that may involve the proceeds of corruption, and such engagements should be subjected to EDD.

The Narcotic Drugs and Psychotropic Substances Act, 1985: regulates narcotic drugs and psychotropic substances and provides for the prevention and punishment of drug trafficking offences. Chartered accountants should assess whether clients or transactions present links to drug trafficking or its proceeds.

The Fugitive Economic Offenders Act, 2018: It targets high-value financial criminals and provides for the confiscation of properties of those who evade criminal prosecution by remaining outside India. Chartered Accountants acting on behalf of clients undertaking cross-border transactions should verify the identity and beneficial ownership.

The Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015: The Act provides provisions to deal with undisclosed foreign income and assets held by Indian residents. For Chartered Accountants undertaking transactions for clients with overseas financial assets, such engagements should be subject to EDD and risk assessment.

The Foreign Contribution (Regulation) Act, 2010: It regulates the acceptance and utilisation of foreign contribution. Chartered accountants acting on behalf of clients receiving foreign contributions should assess whether the transaction complies with the Act and perform risk assessment and EDD when required.

The Conservation of Foreign Exchange and Prevention of Smuggling Activities Act, 1974 (COFEPOSA): Provides for detention of persons engaged in smuggling and foreign exchange violations for prevention. It is relevant where transactions involve clients with potential links to such activities. These engagements should be subject to CDD and beneficial ownership verification to ensure the value involved is not proceeds of crime.

The Smugglers and Foreign Exchange Manipulators (Forfeiture of Property) Act, 1976 (SAFEMA): Provides for the seizure of illegally acquired property derived from smuggling and foreign exchange violations. It forms part of the legal framework for identifying and managing ML risks associated with such property. CA’s Notified transactions should be assessed to ensure they are not used to conceal, transfer or legitimise such property through corporate or financial structures.

The Arms Act, 1959: Implements a framework for regulating arms and ammunition. For Chartered accountants, it is relevant where notified engagements involve clients in the arms sector. Such engagements should be subject to appropriate risk assessment and may require enhanced due diligence and sanctions screening.

The Chemical Weapons Convention Act, 2000: Regulates activities involving scheduled chemicals and supports India’s counter-proliferation financing framework. For chartered accountants, it is relevant when undertaking notified transactions for clients dealing with controlled chemicals, requiring risk assessment and CDD for potential proliferation risks.

The Central Vigilance Commission Act, 2003: The anti- corruption framework establishing the Central Vigilance Commission to detect and investigate corruption. Although it does not impose direct AML obligations on chartered accountants, it highly supports the PMLA framework.

Core AML/CFT/CPF Obligations for Chartered Accountants in India

Where a chartered accountant carries out the specified financial transactions for a client, the regulations require the member to undertake the following. This article keeps each at the level required by law; a compliance requirements guide explains how to do each.

- Register with FIU-IND. Enrol with the Financial Intelligence Unit – India on the FINnet 2.0 / FINGate 2.0 portal once the member begins carrying out the notified financial transactions for clients, so the relevant person can file its reports.

- Appoint officers. Appoint a Designated Director and a senior-level Principal Officer under Rule 7 of the PMLR. The same person cannot hold both roles, and both are to be informed to FIU-IND.

- Conduct the internal risk assessment. Assess money-laundering, terrorist financing and proliferation financing risk across client types, the notified services and geographies, drawing on the FATF accounting-profession guidance, and keep it current.

- Document AML policy, controls and procedures. Adopt an approved policy that turns the risk assessment into the practice’s operating procedures, as required by the joint Guidelines.

- Client identification and CDD. Identify and verify every client and the beneficial owner (a controlling interest of more than 10 per cent for a company or partnership, and more than 15 per cent for an unincorporated association or body of individuals), with enhanced due diligence for politically exposed persons and high-risk clients, under Section 11A of the PMLA, Rule 9 of the PMLR and the joint Guidelines, using the officially valid documents the Guidelines list.

- Ongoing monitoring and periodic update. Monitor the engagement on an ongoing basis, and refresh KYC at least once every 2, 8 and 10 years for high, medium and low-risk clients. Review each client’s risk categorisation at least once every six months and decide whether enhanced due diligence is required.

- Sanctions screening. Screen clients and beneficial owners against the designated lists under Section 51A of the UAPA and Section 12A of the WMD Act, and freeze and report any match. Verify the relevant UNSC and domestic designated lists daily. This duty attaches to each notified engagement.

- Regulatory reporting. File suspicious transaction reports of any value, including attempted transactions, promptly once the Principal Officer is satisfied that a transaction is suspicious, under Rule 8(2) of the PMLR. Where a member handles cash in the notified transaction, cash transaction reports for cash over Rupees 10 lakh and reports on counterfeit or forged instruments are filed monthly by the 15th day of the succeeding month, under Rule 3.

- Record management, CKYCR and FINnet 2.0. Keep transaction records for five years from the date of the transaction, and keep identity records and business correspondence for five years after the business relationship ends, under Section 12 of the PMLA. Upload client KYC records to the Central KYC Records Registry under Rule 9A, reuse an existing record where applicable, and file all prescribed reports through FINnet 2.0.

- Training and awareness. Train partners and staff by role to apply the controls and recognise the red flags that arise in the notified engagements.

- Independent testing and audit. Test the programme through internal review or independent assessment, and close every finding.

What this article does not cover

This article explains the laws and regulatory instruments that apply to a chartered accountant acting as a relevant person. It focuses on the AML, CFT and CPF obligations, but it is not a step-by-step compliance manual and does not cover the broader professional and ethical standards that the ICAI sets, except where they are relevant to the AML duties. For implementation, the professionals should separately document policies and programmes covering client acceptance, KYC,CDD, beneficial-owner identification, sanctions screening, transaction monitoring, suspicious transaction reporting, staff training, audit and management oversight. These operational controls are discussed in the companion compliance guide.

To understand how the professional framework fits within the wider AML regime, see AML laws and regulations in India, and use the parent overview, AML laws and regulations for DNFBPs in India, to see how the professionals sit alongside the other designated businesses.

From regulation to compliance: your next step

Understanding the legal framework is only the first step. Compliance is achieved when those legal obligations are translated into a practical implementation of risk assessment, policy, client due diligence, monitoring, screening, reporting, training and independent review. Because the obligations arise only when there is a specific engagement, the safest approach is to identify at the acceptance stage whether the engagement involves a notified transaction and apply the programme to those from the outset. Understanding the three stages of money laundering and how the sanctions screening process works is a useful starting point.

Not sure which of your mandates are notified transactions?

AML India can help a practice identify which engagements bring it within the PMLA and build a proportionate programme for those.

Frequently Asked Questions

A chartered accountant becomes a reporting entity when, in practice and on behalf of a client, the certificate holder carries out one of the mentioned financial transactions. These transactions include buying or selling immovable property; managing client money, securities or other assets; managing bank, savings or securities accounts; organising contributions for the creation, operation or management of companies; or the creation, operation or management of companies, LLPs or trusts and the buying and selling of business entities.

No. Chartered accountants do not become reporting entities merely by engaging in the work that defines the profession, including Statutory audit, tax audit, certification and attestation services, representation and ordinary compliance filings. Reporting entity obligations arise only when the CA is handling or arranging a client’s money, assets, accounts or corporate vehicles.

The Institute of Chartered Accountants of India(ICAI) supervises chartered accountants for AML compliance under the joint AML and CFT Guidelines issued for ICAI, ICSI and ICMAI professionals. Reports are submitted to the Financial Intelligence Unit – India, while the Enforcement Directorate investigates and prosecutes the offence of money laundering.

No. A chartered accountant is covered when, in the course of practice and on behalf of a client, they undertake a notified transaction, irrespective of its value. The trigger is the nature of the activity, not the value.

A CA must file suspicious transaction reports for suspicious or attempted suspicious transactions, irrespective of their value. Where notified engagements involve cash, they must file cash transaction reports for cash over Rupees 10 lakh and reports on counterfeit or forged instruments.

Yes. The screening duties under Section 51A of the UAPA and Section 12A of the WMD Act apply whenever the member acts as a relevant person, from the start of a notified engagement. The member screens clients and beneficial owners against the designated lists and freezes and reports any match, whatever the value of the work.

Chartered Accountants balance AML reporting with client confidentiality by complying with both their professional obligations and PMLA. Client confidentiality remains the general rule, but the PMLA creates an exception for the notified engagements where reporting obligations apply. The joint Guidelines and the ICAI FAQs explain how a member manages these, so professional confidentiality and the reporting duty can both be met.

A chartered accountant who carries out specified financial transactions for a client, such as handling client money, forming or managing companies, or dealing in property, is a reporting entity under Section 2(1)(sa) of the PMLA. The requirements then include registering with FIU-IND, appointing a Principal Officer and Designated Director, performing customer due diligence, keeping records for five years and reporting suspicious transactions. Pure audit and tax work does not trigger these duties.

Yes. The ICAI issued joint anti money laundering guidelines for the profession on 19 June 2023, which sit under the PMLA and the PML (Maintenance of Records) Rules, 2005. They explain when a chartered accountant is covered, what customer due diligence and record keeping to perform, and the red flags to watch for. They are the primary anti money laundering guidance for the accountancy sector in India.

Verify the client’s identity on officially valid documents, understand the purpose of the engagement, and identify the ultimate beneficial owner before acting. Screen for red flags such as unexplained cash, opaque ownership structures or evasive answers, and monitor the engagement as it proceeds. Document each check, because the record is what demonstrates compliance.

Official sources and review

Last reviewed: July 2026. This guide is grounded in the following primary official sources, linked to their official source where available.

- Prevention of Money-Laundering Act, 2002 (India Code)

- Prevention of Money-Laundering (Maintenance of Records) Rules, 2005 (India Code)

- Notification S.O. 2036(E), 3 May 2023, notifying the specified financial transactions (Gazette of India)

- AML/CFT Guidelines for professionals with certificates of practice from ICAI, ICSI and ICMAI, 19 June 2023 (ICAI)

- Chartered Accountants Act, 1949 (India Code)

- Unlawful Activities (Prevention) Act, 1967 and Section 51A procedure (MHA)

- WMD Act, 2005 and its Section 12A implementation procedure (India Code)

- FATF Recommendations, including the June 2026 update to Recommendation 6

- FATF Risk-Based Approach Guidance for the Accounting Profession, 2019

- FATF Mutual Evaluation Report on India, 2024

- Financial Intelligence Unit – India, including the Annual Report 2024-25

- Enforcement Directorate annual report 2025-26

Why work with AML India

AML India helps chartered accountants in practice comply with their obligations under PMLA for notified engagements, covering every stage of the compliance lifecycle from registration and risk assessment to CDD, screening, monitoring, training and independent review.

Industries we serve: Chartered Accountants, Company Secretaries and Cost and Management Accountants, Trust and Company Service Providers, Real Estate Agents, Dealers in Precious Metals and Stones, Virtual Asset Service Providers, Casinos and the Gaming Sector, and Banks, Financial Institutions and IFSC and GIFT City entities.

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is a Chartered Accountant with more than 26 years of experience in governance, risk, and compliance. He helps companies with end-to-end AML compliance services, from conducting Enterprise- Wide Risk Assessments to implementing the robust AML Compliance framework. He has played a pivotal role as a functional expert in developing and implementing RegTech solutions for streamlined compliance.

Reach Out to Pathik