Quick Overview

• India’s AML/CFT guidelines for Trust and Company Service Providers (TCSPs) came into effect on 21 April 2026, following the Central Government’s notification S.O. 2135(E) dated 9 May 2023.

• TCSPs are now classified as Reporting Entities (REs) under the Prevention of Money Laundering Act, 2002 (PMLA).

• The guidelines are issued by the Financial Intelligence Unit India (FIU-IND) and cover five specific activities carried out in the course of business, on behalf of or for another person.

• Obligations include ML/FT risk assessment, AML/CFT policies and procedures, KYC, Client Due Diligence, Enhanced Due Diligence, sanctions screening, suspicious transaction reporting, and record-keeping.

• The regulatory framework draws from PMLA 2002, PMLR 2005, UAPA 1967, and the WMD Act 2005.

On 9 May 2023, the Central Government issued a notification (S.O. 2135(E)) that brought Trust and Company Service Providers (TCSPs) under the Prevention of Money Laundering Act, 2002 (PMLA). The notification identified five specific services that TCSPs typically provide, such as forming companies, acting as directors or trustees, and holding nominee shares. Anyone carrying out these services on behalf of another person is now classified as a Reporting Entity (RE) under PMLA.

The AML & CFT Guidelines for Trust and Company Service Providers (TCSPs), issued by the Financial Intelligence Unit India (FIU-IND), summarise the anti-money laundering (AML), counter-terrorism financing (CFT), and counter-proliferation financing (CPF) obligations that apply to TCSPs. They draw from PMLA 2002, the Unlawful Activities (Prevention) Act 1967, the Weapons of Mass Destruction Act 2005, and the rules and notifications issued under these laws.

The guidelines took effect on 21 April 2026. From this date, every TCSP that performs any of the five notified activities must comply with PMLA’s full set of requirements, including ML/FT risk assessment, policy and procedures drafting, record-keeping, client verification, due diligence, and suspicious transaction reporting.

In simple terms, TCSPs must now know who their clients are, understand the risks involved, keep proper records, and report anything suspicious to FIU-IND.

Who is a TCSP Under India's AML Framework?

The definition is activity-based. If a business carries out any of the following on behalf of or for another person, in the course of business, it qualifies as a Relevant Person under the guidelines.

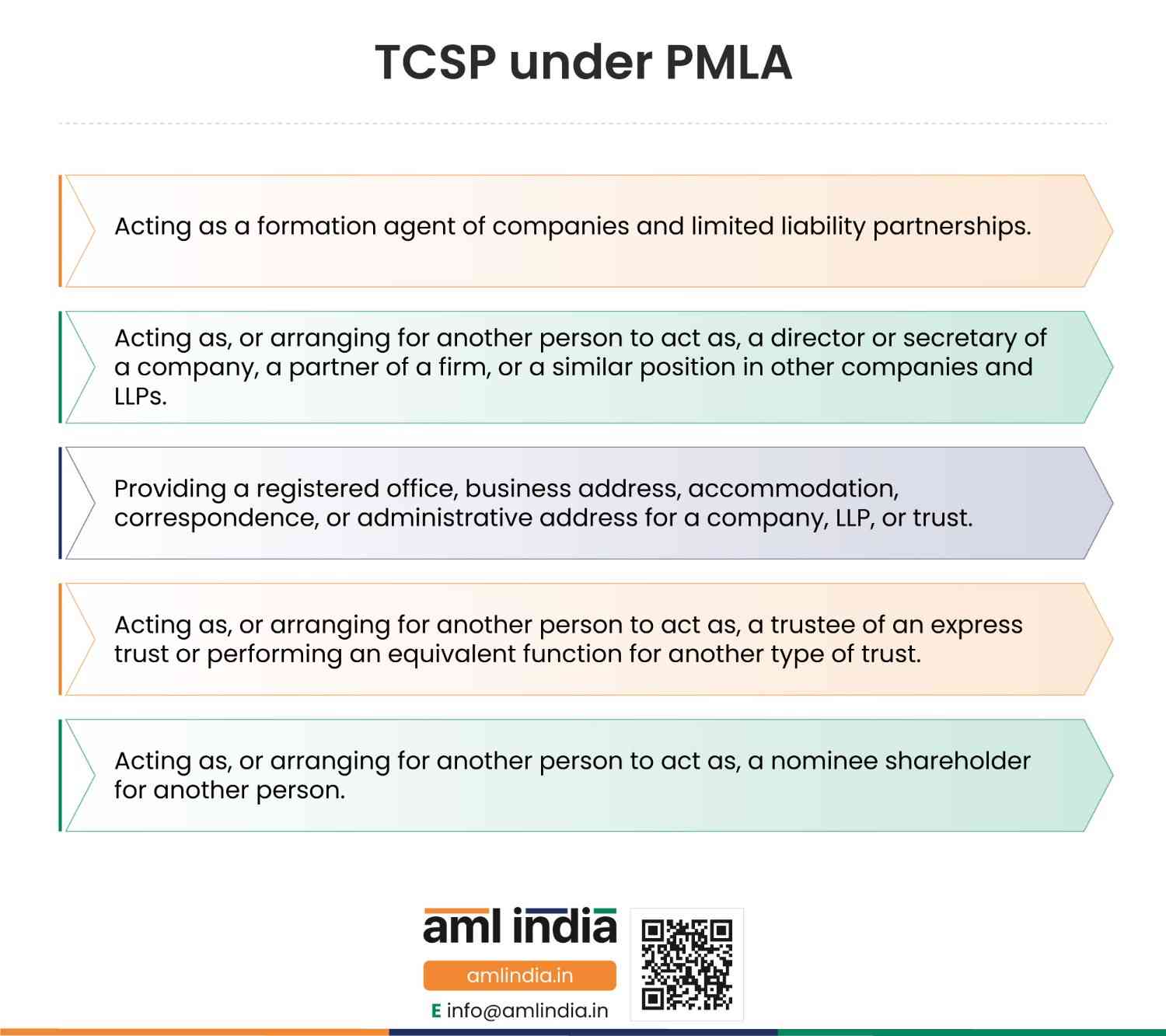

The Five Notified Activities

- Acting as a formation agent of companies and limited liability partnerships.

- Acting as, or arranging for another person to act as, a director or secretary of a company, a partner of a firm, or a similar position in other companies and LLPs.

- Providing a registered office, business address, accommodation, correspondence, or administrative address for a company, LLP, or trust.

- Acting as, or arranging for another person to act as, a trustee of an express trust or performing an equivalent function for another type of trust.

- Acting as, or arranging for another person to act as, a nominee shareholder for another person.

What Does Not Count

The guidelines are equally clear about what falls outside the scope:

- Any activity under a lease, sub-lease, tenancy, or any other agreement or arrangement for the use of land or building or any space, where the consideration is subject to TDS under Section 194-I of the Income Tax Act, 1961.

- Any activity carried out by an employee on behalf of their employer in the course of employment.

- Any activity by an advocate, chartered accountant, cost accountant, or company secretary engaged in company formation solely to the extent of filing a declaration under Section 7(1)(b) of the Companies Act, 2013.

- Any activity of a person who qualifies as an intermediary under Section 2(1)(n) of the PMLA.

Key AML/CFT Terms for TCSPs in India

Term | Full Form | What It Means in Practice |

AML | Anti-Money Laundering | Laws, controls, and procedures to prevent the conversion of criminal proceeds into legitimate assets. |

CFT | Countering the Financing of Terrorism | Measures to detect and prevent funds from reaching terrorist individuals or organisations. |

CPF | Combating Proliferation Financing | Controls targeting the financing of weapons of mass destruction and their delivery systems. |

PMLA | Prevention of Money Laundering Act, 2002 | The primary AML legislation in India, governing all Reporting Entities. |

PMLR | Prevention of Money Laundering (Maintenance of Records) Rules, 2005 | Operational rules under PMLA covering record-keeping, reporting, and CDD procedures. |

RE | Reporting Entity | Any entity classified under PMLA as having AML/CFT obligations, now including TCSPs. |

FIU-IND | Financial Intelligence Unit India | The central national agency receiving, processing, and disseminating financial intelligence. |

KYC | Know Your Customer | Process of identifying and verifying the identity of a client before and during a business relationship. |

CDD | Customer Due Diligence | Broader measures to understand the client, their business, and the nature of the relationship. |

EDD | Enhanced Due Diligence | More rigorous checks applied to higher-risk clients, transactions, or jurisdictions. |

RBA | Risk-Based Approach | Allocating compliance resources proportionate to the level of ML/TF/PF risk identified. |

PEP | Politically Exposed Person | Individuals entrusted with prominent public functions by a foreign country. The enhanced due diligence requirements also apply to their family members and close associates. |

STR | Suspicious Transaction Report | A report filed with FIU-IND when a transaction is suspected to involve ML/TF/PF. |

OVD | Officially Valid Document | Government-issued identity documents accepted for KYC purposes under PMLR. |

CKYCR | Central Know Your Customer Registry | A centralised repository of KYC records maintained by the Government of India. |

UAPA | Unlawful Activities (Prevention) Act, 1967 | Legislation covering terrorism-related offences, including obligations to check UNSC sanctions lists. |

WMDA | Weapons of Mass Destruction and Delivery Systems (Prohibition of Unlawful Activities) Act, 2005 | Legislation governing proliferation financing obligations for Reporting Entities. |

The Legal Framework: Laws That Govern TCSP Compliance in India

TCSP compliance in India does not rest on a single regulation. It draws from a layered body of law, each piece adding a distinct obligation.

Prevention of Money Laundering Act, 2002 (PMLA)

In force since 1 July 2005, PMLA is the foundation. Section 11A requires REs to verify the identity of clients and beneficial owners. Section 12 imposes obligations to maintain transaction records, furnish information to FIU-IND, and retain client identity and correspondence documents. Section 12A empowers the Director, FIU-IND, to call for any information from REs as required.

Prevention of Money Laundering (Maintenance of Records) Rules, 2005 (PMLR)

The operational engine of PMLA. Rule 3 prescribes which transactions must have records maintained. Rule 7 covers the procedure for furnishing information to FIU-IND and requires REs to build internal detection mechanisms. Rule 8 sets reporting timelines. Rule 9 lays out the Client Due Diligence procedure, including beneficial owner identification and verification.

Unlawful Activities (Prevention) Act, 1967 (UAPA)

Section 51A of UAPA requires REs to ensure that no client appears on the UNSC-approved lists of individuals and entities suspected of terrorist links. The ISIL/Al-Qaida Sanctions List and the Taliban Sanctions List must be verified daily. Any match must be reported to FIU-IND and the Ministry of Home Affairs.

Weapons of Mass Destruction and Delivery Systems (Prohibition of Unlawful Activities) Act, 2005 (WMD Act)

Section 12A of the WMD Act, operationalised through a Ministry of Finance order dated 1 September 2023, requires REs to check clients against the designated proliferation financing list, prevent any matching transaction, and report immediately to the Central Nodal Officer (designated as the Director, FIU-India). REs must also comply with any asset freeze order issued by the CNO under Section 12A of the WMD Act.

Notification S.O. 2135(E) dated 9 May 2023

The Central Government notification that formally brought TCSPs within the PMLA framework by notifying the five activities described in Section 2. This is the entry point that makes all of the above applicable to the sector.

General Obligations of Relevant Persons

AML/CFT/CPF Programme

Every RE must have a functioning AML/CFT/CPF programme in place. Rule 7(3) of PMLR requires REs to build an internal mechanism capable of detecting transactions specified under Rule 3(1) and reporting them to FIU-IND. The programme must be calibrated to the size and nature of the business, but it must exist, and it must work.

Internal Policies, Procedures, and Controls

REs must issue a written statement of policies and procedures addressing ML, TF, and PF risks, reviewed periodically to confirm they remain current with statutory and regulatory requirements. This includes a formal client acceptance policy, written CDD procedures, and, for entities operating within a group structure, group-wide policies implemented in accordance with Rule 3A of PMLR.

Registration, Designated Director, and Principal Officer

Two appointments are mandatory and must be with separate individuals.

The Designated Director holds overall responsibility for compliance with Chapter IV of PMLA and the Rules.

The Principal Officer (PO) sits at the management level, preferably not below the level of Head of Audit/Compliance or Chief Risk Officer, and is responsible for day-to-day implementation. Both must be communicated to FIU-IND promptly.

The Principal Officer is responsible for filing STRs, evolving the internal detection mechanism, communicating AML/CFT/CPF policies across the organisation, and ensuring records are maintained, and law enforcement cooperation is provided where required.

Internal Control and Audit

REs must subject their AML/CFT/CPF policies, procedures, and controls to regular internal audit. The audit function exists to verify that the programme is not only documented but genuinely operational, catching gaps before a regulator does.

KYC, CDD, and EDD

Know Your Customer (KYC) Norms

All REs must have a robust mechanism for KYC at the time of client onboarding, as well as for re-KYC and continued due diligence of existing clients. Services must not be provided under anonymous, pseudonymous, or fictitious names.

For KYC purposes, PAN (for residents) or an equivalent document (for non-residents), together with any of the following Officially Valid Documents (OVDs), may be used:

- Passport

- Driving licence

- Proof of possession of the Aadhaar number

- Voter’s Identity Card issued by the Election Commission of India

- Job card issued by NREGA, duly signed by an officer of the State Government

- A letter issued by the National Population Register containing name and address details

Where the OVD furnished by the customer does not have an updated address, the following documents may be accepted as proof of address: a utility bill not more than two months old (electricity, telephone, post-paid mobile phone, piped gas, or water), a property or municipal tax receipt, a pension or family pension payment order issued by a Government Department or Public Sector Undertaking (if it contains the address), or a letter of allotment of accommodation from an employer issued by a Government Department, statutory or regulatory body, public sector undertaking, scheduled commercial bank, financial institution, or listed company. The customer must submit an OVD with a current address within three months of submitting these documents.

Where the OVD presented by a foreign national does not contain address details, documents issued by the government departments of foreign jurisdictions or a letter issued by the Foreign Embassy or Mission in India may be accepted as proof of address.

Where e-KYC services of UIDAI are used, biometric authentication (finger/iris) serves as the primary mode, with OTP-based authentication as a second factor, subject to the client’s specific and express consent.

In addition to record-keeping and reporting requirements under PMLA and PMLR, TCSPs must also comply with relevant record-keeping and reporting requirements under the Information Technology Act and the Income Tax Act.

For legal persons, KYC must also establish the name, legal form, proof of existence, powers that regulate and bind the entity, and the address of the registered office or main place of business.

Periodic Updation of KYC

REs must adopt a risk-based approach to KYC updation, ensuring data collected under CDD remains current. Minimum updation timelines are as follows:

Risk Category | KYC Updation Frequency |

High-Risk Customers | At least once every two years |

Medium-Risk Customers | At least once every eight years |

Low-Risk Customers | At least once every ten years |

Where CDD measures cannot be applied, or identity cannot be ascertained, or information appears false or non-genuine, the RE must not enter into the engagement and must file a suspicious activity report with FIU-IND.

Client Due Diligence (CDD) Norms

REs must maintain accurate and up-to-date client information and adopt written procedures for the Client Due Diligence process under Rule 9 of PMLR. CDD measures must include:

- Robust due diligence on clients, beneficial owners, authorised signatories, and counterparties.

- Financial and criminal background checks for international clients prior to accepting the engagement.

- Identification of risk-related details through sanctions screening providers.

- Retention of KYC and identification documents for at least five years.

- Submission of reports to FIU-IND on a timely basis or upon request.

- Ongoing CDD measures are determined on a risk-sensitive basis, recognising that ML/TF/PF risks may change as a business relationship develops.

Specific documents required by entity type:

For a Company

- Certificate of incorporation

- Memorandum and Articles of Association

- Permanent Account Number of the company

- Board resolution and power of attorney granted to managers, officers, or employees

- Documents relating to beneficial owners and those holding power of attorney

- Names of persons in senior management positions and the principal place of business

For a Partnership Firm

- Certificate of incorporation

- Memorandum and Articles of Association

- Permanent Account Number of the firm

- Board resolution and power of attorney granted to managers, officers, or employees

- Documents relating to beneficial owners and those holding power of attorney

For a Trust

- Registration certificate

- Trust deed

- Permanent Account Number or Form No. 60 of the trust

- Documents relating to beneficial owners, managers, officers, or employees holding power of attorney

- Names of beneficiaries, trustees, settlor, protector (if any), and authors of the trust

- Address of the registered office of the trust

- List of trustees and documents for those authorised to transact on behalf of the trust

For non-profit organisation clients, REs must confirm that the customer is registered on the DARPAN Portal of NITI Aayog and retain such registration records for five years after the relationship ends.

Enhanced Due Diligence (EDD)

Where risks of ML/TF/PF are higher, REs must conduct enhanced due diligence commensurate with the risk identified. EDD is not limited to collecting additional income proofs. It means measures that are more rigorous and robust than standard KYC, including:

- More frequent review of the client’s profile and transactions.

- Gathering information from publicly available sources or otherwise.

- Reasonable measures to establish the client’s source of funds.

- Conducting independent enquiries on details provided by the client.

- Consulting credible databases, public or otherwise.EDD must be applied in the following situations in particular:

EDD must be applied in the following situations in particular:

- Business relationships and transactions with natural or legal persons from higher-risk jurisdictions, including FATF grey and black list countries and tax havens.

- Business relationships with Politically Exposed Persons (PEPs), as defined under Rule 2(1)(db) of PMLR.

Staff handling sensitive information must be well-trained specifically to prevent internal tipping-off.

Beneficial Owner Identification

REs must identify the beneficial owner(s) and take all reasonable steps to verify their identity, as required under Rule 9(3) of PMLR. The beneficial owner is determined as follows:

Where the Customer is a Company

The beneficial owner is the natural person(s) with controlling ownership interest (more than 10% of shares, capital, or profits) or who exercises control through other means (including the right to appoint the majority of directors, or control through shareholder or voting agreements). Where no natural person meets the threshold, the institution must identify any person exercising control through other means. Where no such person can be identified, the Senior Managing Official (such as the CEO or Managing Director) is recorded as the beneficial owner. REs may lower the 10% threshold for companies incorporated in high-risk jurisdictions.

Where the Customer is a Partnership Firm

The beneficial owner is the natural person(s) with ownership or entitlement to more than 10% of the capital or profits of the partnership, or who exercises control through other means, including control over management or policy decisions.

Where the Customer is a Trust

Beneficial owner identification must include the author of the trust, all trustees, beneficiaries with 10% or more interest in the trust, and any other natural person exercising ultimate effective control over the trust.

Politically Exposed Persons (PEPs)

PEPs are individuals who are or have been entrusted with prominent public functions by a foreign country, including Heads of State or Government, senior politicians, senior government officials, judicial or military officers, senior executives of state-owned corporations, and important political party officials.

REs may establish relationships with PEPs provided that:

- Appropriate risk management systems are in place to identify whether the customer or beneficial owner is a PEP.

- Reasonable measures are taken to establish a source of funds and wealth.

- All PEPs are subject to enhanced monitoring on an ongoing basis.

- These requirements extend to family members and close associates of PEPs.

Sanctions Screening

Sanctions screening must be carried out at the time of onboarding and whenever any of the notified activities are conducted. REs must ensure prompt application of directives issued by competent authorities relating to UNSC resolutions, national sanctions, and all other applicable regulatory requirements on economic sanctions.

UAPA Obligations

Under Section 51A of UAPA, REs must ensure no client appears on the following UNSC lists, which must be verified daily:

- The ISIL (Da’esh) and Al-Qaida Sanctions List, established under Security Council Resolutions 1267/1989/2253.

- The Taliban Sanctions List, established under Security Council Resolution 1988 (2011).

REs must also refer to the lists in the Schedules to the Prevention and Suppression of Terrorism (Implementation of Security Council Resolutions) Order, 2007. Any match must be reported to FIU-IND and the Ministry of Home Affairs as required under the UAPA notification dated 2 February 2021. Where a match is found, REs must also comply with the asset freezing procedures set out in the UAPA Order dated 2 February 2021. A list of Nodal Officers designated for UAPA compliance is available on the MHA website.

WMD Act Obligations

Under Section 12A of the WMD Act, 2005, REs must:

- Not carry out transactions where the client’s particulars match those on the designated list.

- Run checks at the time of establishing a client relationship and periodically thereafter.

- Where a match is found, immediately inform the Central Nodal Officer (Director, FIU-India) with full particulars of funds and assets involved.

- Prevent the individual or entity from conducting transactions and notify the CNO by email, fax, and post without delay where there is doubt that assets would fall under Section 12A(2) of the WMD Act.

- Comply with any asset freeze order received from the CNO without delay.

- Forward applications for unfreezing, together with full asset details, to the CNO within two working days.

- Verify the UNSCR 1718 Sanctions List of Designated Individuals and Entities every day.

The designated list is available on the FIU-India portal and must be monitored for additions, deletions, and other changes on a daily basis. REs must also take into account other relevant UN Security Council Resolutions and the lists in the first and fourth schedules of UAPA 1967 when complying with Government orders on implementation of Section 51A of UAPA and Section 12A of the WMD Act.

FATF Non-Compliant Jurisdictions

REs must apply enhanced due diligence, effective and proportionate to the risks, to business relationships and transactions with persons from countries identified in FATF statements as not or insufficiently applying FATF Recommendations.

The background and purpose of all such transactions must be examined, and written findings must be retained and made available to relevant authorities on request.

These screening requirements do not preclude REs from having legitimate trade and business relationships with persons in the listed countries. REs are encouraged to leverage technological tools for effective and efficient name screening.

Transaction Monitoring and Suspicious Transaction Reporting

REs must monitor all transactions carried out on behalf of their clients, including transactions by counterparties. An effective transaction monitoring system must be developed, implemented, and maintained to enable the detection of possible ML/TF/PF activity.

REs are mandated to keep records of alerts generated based on Red Flag Indicators issued by FIU-IND and to document the action taken on each alert. IP address tracking and digital footprint analysis may be incorporated for clients who interact primarily through digital or correspondence addresses.

When to File a Suspicious Transaction Report

Where a RE has reasonable grounds to suspect that funds are connected to criminal activity, or are proceeds of crime, or are related to ML, TF, or PF, it must file a Suspicious Transaction Report (STR) promptly with FIU-IND in the manner prescribed.

Critically, there is no threshold: REs must file an STR regardless of the transaction amount or any threshold limit envisaged under PMLA, if there are reasonable grounds to believe the transaction involves proceeds of crime.

Suspicious transactions must be reported promptly upon forming suspicion, in accordance with Rule 8(2) read with Rule 3(1)(D) of PMLR. This includes attempted transactions, whether or not made in cash.

Special attention must be paid to complex transactions, unusually large transactions, and all unusual patterns with no apparent economic or visible lawful purpose. The background of such transactions, including all documents, office records, and memoranda, must be examined by the Principal Officer and findings recorded.

Record-Keeping, Confidentiality, and Tipping-Off

Record-Keeping

Record Type | Retention Period |

Identity and beneficial owner documents, account files, and business correspondence | Five years after the business relationship ends or the account is closed, whichever is later |

Transaction records | Five years from the date of the transaction |

Records relating to ongoing investigations or disclosures | Until confirmed that the case is closed |

PML Rules records (general) | Ten years from the date of cessation of transactions between client and RE |

REs must also implement procedures for retaining internal records of both domestic and international transactions in a manner that enables reconstruction of individual transactions, sufficient to provide evidence for prosecution of criminal activity if required.

Confidentiality

REs, their directors, officers, and employees must ensure that the maintenance of records under PML Rules and the furnishing of information to the Director, FIU-IND, is kept strictly confidential.

REs must also have adequate safeguards in place to prevent unauthorised access to, alteration of, destruction of, or dissemination of records and information. Physical and electronic access to such records must be controlled and monitored, and REs must establish standard transmission and encryption formats for data shared with authorities.

Prohibition on Tipping-Off

REs and their directors, officers, and employees (permanent and temporary) are prohibited from disclosing that an STR or related information is being considered, reported, or provided to FIU-IND. This prohibition applies before, during, and after the submission of an STR. There must be no tipping-off to the client at any level.

Risk Assessment

REs must carry out a periodic ML/TF/PF risk assessment exercise to identify, assess, and mitigate their money laundering, terrorist financing, and proliferation financing risk. Risk assessments must be designed to identify priority areas for resource allocation and appropriate oversight of AML/CFT/CPF activities.

REs must identify areas where their products, services, or client base could be exposed to ML/TF/PF risks, taking into account factors such as the types of clients served, services offered, countries of operation, and publicly available information on ML/TF/PF trends. Customers carrying out extremely complex or unusually high-value transactions must be flagged for closer review.

The risk assessment must cover four main categories:

- Country or geographic risk

- Customer or counterparty risk

- Product or service risk

- Delivery channels risk

The periodicity of the risk assessment exercise is determined by the Board or any delegated committee, but must be reviewed at least annually. The outcome must be placed before the Board and made available to competent authorities upon request.

REs must apply a Risk-Based Approach (RBA) for mitigation and management of identified risks, supported by Board-approved policies, controls, and procedures. Client risk categorisation must be built into client acceptance procedures, covering at a minimum three categories: high risk, medium risk, and low risk. Factors of risk perception for monitoring suspicious transactions must be clearly defined, having regard to the client’s location, nature of business activity, trading turnover, and manner of payment.

Specific client categories warranting dedicated risk assessment include non-residents, high net worth individuals, trusts, PEPs, charities, NGOs, organisations receiving donations, companies with close family shareholding or beneficial ownership, and firms with sleeping partners.

Where the identity of a client is ascertained as having a criminal background, a suspicious transaction report must be filed with FIU-IND.

The risk assessment must be documented, kept up-to-date, and made available to the Director, FIU-IND, as and when required. Client engagements must not be entered into under fictitious names or accounts belonging to persons whose identity cannot be verified.

How AML India Can Help TCSPs

Building a compliant AML/CFT/CPF programme from the ground up is not a small undertaking, particularly for TCSPs that are encountering these obligations for the first time.

AML India is a specialist AML compliance services provider focused exclusively on the Indian regulatory environment, with deep expertise in PMLA 2002 and the frameworks that surround it.

Whether you are determining whether the guidelines apply to your business, setting up your programme for the first time, or reviewing the adequacy of existing controls, AML India offers end-to-end support across the full compliance lifecycle.

Service | What It Covers |

AML Policy Documentation | Drafting and implementing AML/CFT/CPF policies, procedures, and controls tailored to your business, client profile, and risk exposure under PMLA 2002. |

AML Business Risk Assessment | Conducting a structured ML/TF/PF risk assessment across your customer base, geographies, products, and delivery channels, documented and Board-ready. |

AML Compliance Department Setup | Setting up an in-house AML compliance function, including support with appointing a Principal Officer and Designated Director, role design, and reporting structures. |

AML Health Check | An independent review of your existing AML/CFT programme against PMLA, PMLR, and the TCSP guidelines to identify gaps and remediation priorities. |

AML Software Selection | Guidance on selecting and implementing the right AML technology for your transaction monitoring, sanctions screening, and KYC workflows. |

AML Training | Bespoke training programmes for management and staff, covering PMLA obligations, typologies, red flag identification, STR filing, and tipping-off controls. |

AML India serves a broad range of regulated entities, including banks and financial institutions, insurance companies, real estate agents, dealers in precious metals and stones, crypto service providers, accountants and legal consultants, securities market intermediaries, and entities operating within the International Financial Services Centre (IFSC) at GIFT City.

Money laundering using trust and company service providers

Money laundering using trust and company service providers is a recognised typology precisely because TCSPs create the legal structures, companies, trusts and nominee arrangements, that can hide the real owner of illicit funds. A launderer can use a TCSP to form a shell company, provide a registered office, or act as a nominee director, putting distance between the criminal and the money. This is why the profession is a designated reporting entity under Section 2(1)(sa) of the PMLA, and why the FIU-IND guidelines for trust and company service providers, effective 21 April 2026, focus so heavily on identifying the ultimate beneficial owner behind every structure the TCSP creates.

How TCSPs meet their AML CFT obligations

TCSP AML compliance is built around beneficial ownership and the purpose of the structure. The provider must register with FIU-IND, appoint a Principal Officer and a Designated Director, and run customer due diligence that looks through the entity to the natural person who ultimately owns or controls it, applying the more than ten per cent test for companies and the more than fifteen per cent test for unincorporated bodies. It must understand why a client wants a particular structure, monitor the relationship, keep records for five years, and report suspicious transactions to FIU-IND. The FIU-IND TCSP guidelines are the sector’s operating manual for these duties.

Frequently Asked Questions

Any business that carries out one or more of the five notified activities (formation agent, director/secretary/partner, registered office provider, trustee, or nominee shareholder) on behalf of another person, in the course of business. The test is activity-based, not licence-based.

The guidelines took effect on 21 April 2026, pursuant to notification S.O. 2135(E) dated 9 May 2023.

CDD is the standard set of measures to identify and verify clients, understand the nature of the relationship, and monitor transactions on an ongoing basis. EDD goes further: it applies where risk is higher and involves more frequent reviews, deeper source-of-funds enquiries, independent background checks, and consulting credible databases. EDD is not simply collecting more documents.

Certificate of incorporation, Memorandum and Articles of Association, PAN of the company, Board resolution and power of attorney, documents relating to beneficial owners and attorneys, and names of senior management and principal place of business.

Client identity and transaction records must generally be retained for five years. PML Rules records must be maintained for ten years from the cessation of transactions. Records relating to ongoing investigations must be kept until the case is confirmed closed.

No. The guidelines explicitly state that REs must file an STR regardless of transaction amount or threshold limit if there are reasonable grounds to believe the transaction involves proceeds of crime.

STRs and other prescribed reports are filed through the FINnet gateway portal (FINgate). Detailed guidance, FAQs, periodic AML/CFT updates, and sanctions screening list updates are available at www.fiuindia.gov.in and www.fingate.gov.in.

Launderers use TCSPs to create companies, trusts and nominee arrangements that obscure the real owner of funds, for example by forming a shell company, supplying a registered office, or acting as a nominee director or shareholder. These structures add layers between the criminal and the money. That risk is why TCSPs are reporting entities under the PMLA and must identify the ultimate beneficial owner behind every structure they create.

TCSPs are reporting entities under Section 2(1)(sa) of the PMLA and follow the FIU-IND guidelines for the sector, effective 21 April 2026. They must register with FIU-IND, appoint a Principal Officer and Designated Director, perform customer due diligence with a strong focus on beneficial ownership, keep records for five years, and report suspicious transactions.

About the Author

Pathik Shah

FCA, CAMS, CISA, CS, DISA (ICAI), FAFP (ICAI)

Pathik is a Chartered Accountant with more than 26 years of experience in governance, risk, and compliance. He helps companies with end-to-end AML compliance services, from conducting Enterprise- Wide Risk Assessments to implementing the robust AML Compliance framework. He has played a pivotal role as a functional expert in developing and implementing RegTech solutions for streamlined compliance.

Reach Out to Pathik